Teaching Content

Tutoring Services Rapid Growth

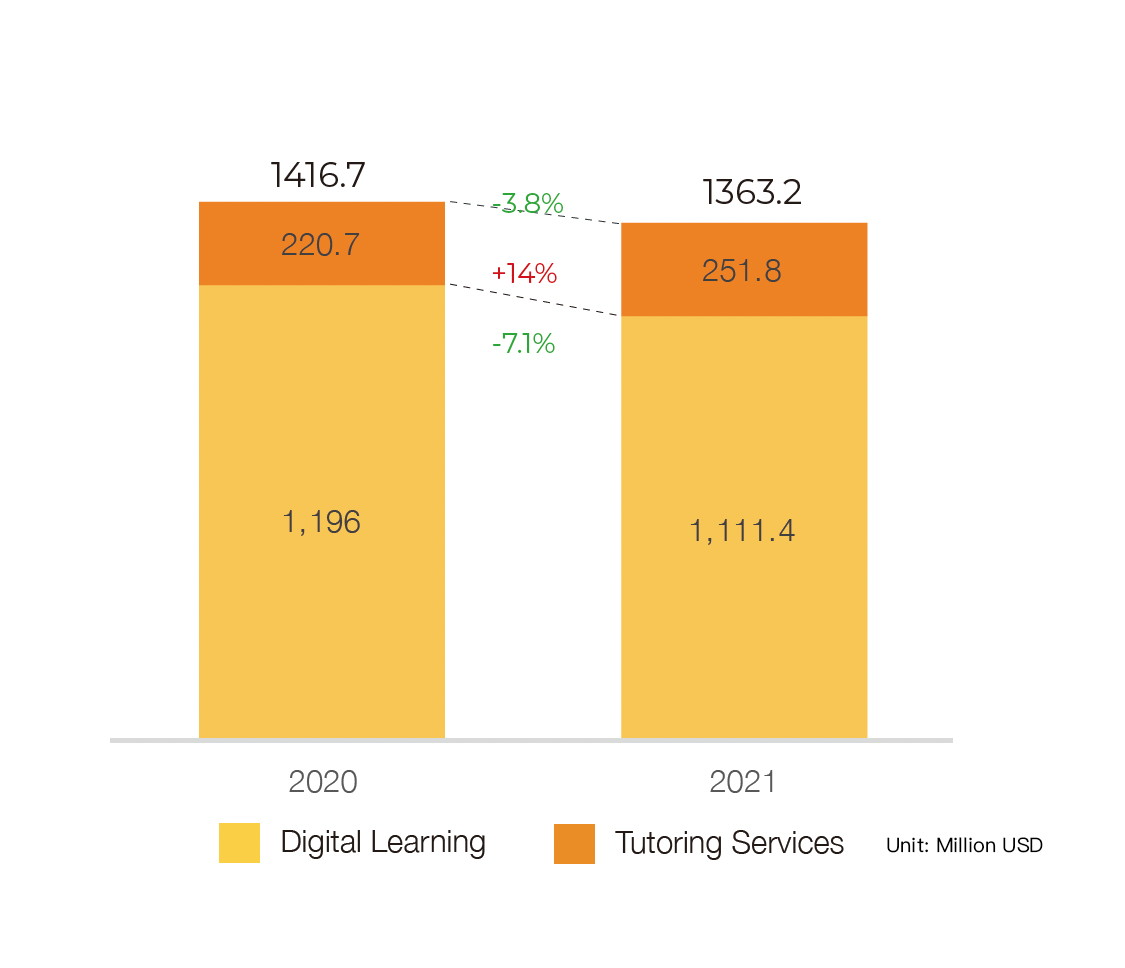

market value of the “Digital Learning” sub-industry. The reason is speculated that it was because the epidemic status in 2020 was properly controlled, and an urgent “online to offline” situation has not yet been created. Moreover, the impacts of COVID-19 on economic life tend to make people more conservative of non-rigid demand consumption decisions, which was unfavorable to the “Digital Learning” development.

Take listed cultural and educational company as an example. Except for a few that can grow against the trend, the operating performance of most businesses in 2020 has been affected by the overall environment and showed a negative growth trend.

In contrast, “Tutoring Services” grew by 14% in 2020. In addition to the relatively small base period, it also indicated that such services are considered emerging services and demands in the industry, which are in a stage of rapid growth.

Software System

Unprecedented Growth

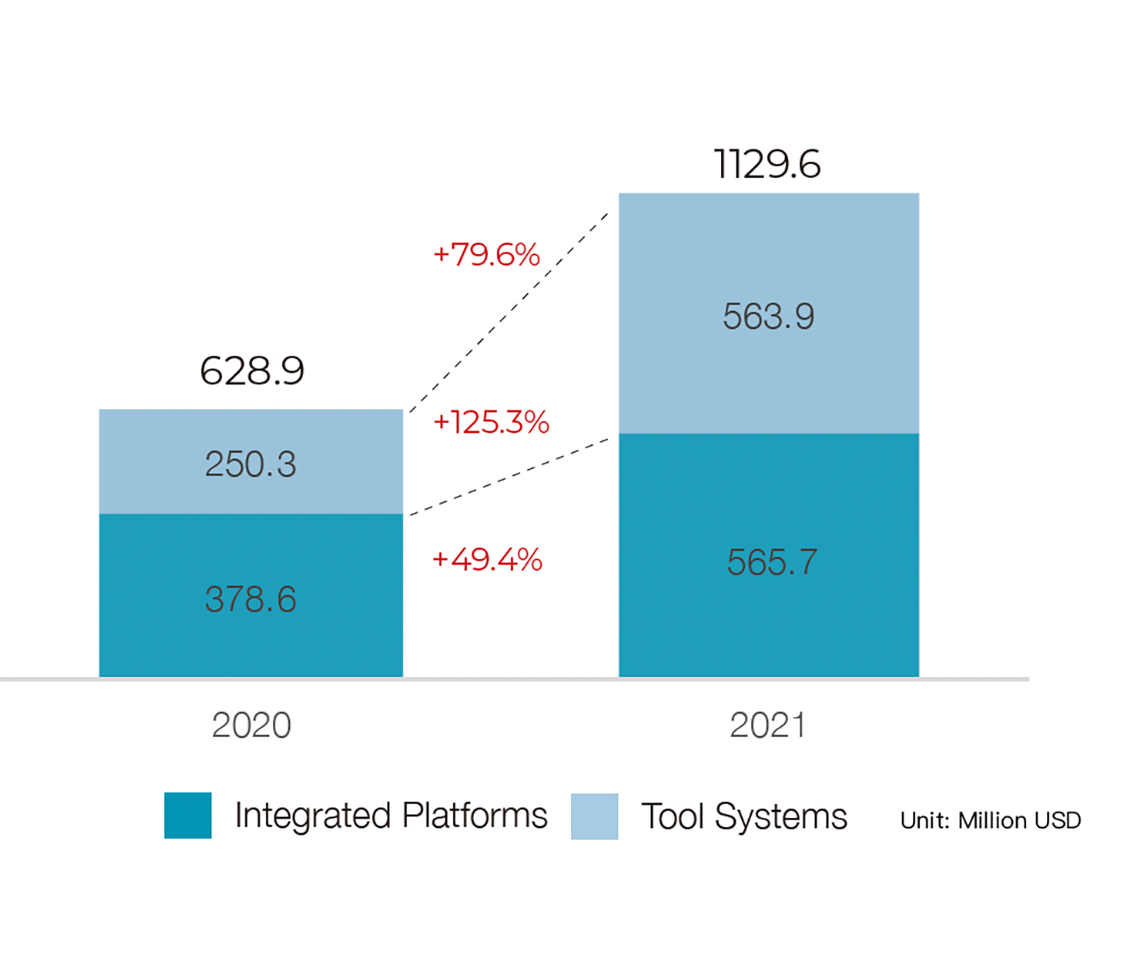

The market value of software systems is US$1,129.6 million, which grew by 79.6% compared to 2020. Among them, the market value of the “Integrated Platforms” sub-industry is US$565.7 million, which accounted for 50.1% of software systems. The market value of the “Tool Systems” sub-industry is US$563.9 million, which accounted for about 49.9% of software systems.

In 2021, the market value of software systems has experienced unprecedented growth momentum and development opportunities. Both “Integrated Platforms” and “Tool Systems” have experienced significant growth. These industry sectors have benefited more from the COVID-19 epidemic. Among them, “Integrated Platforms” cover direct consumer learning platforms (B2C) and institution-oriented platform services (B2B). Since the outbreak of COVID-19 in early 2020, traffic flows for both 2C and 2B platforms have increased for the first time. However, due to differences in revenue models, 2C platforms can convert traffic to revenue faster than that of 2B platforms. Therefore, learning platforms have also become the subject of media coverage during the COVID-19 epidemic and attracted attention from all walks of life.

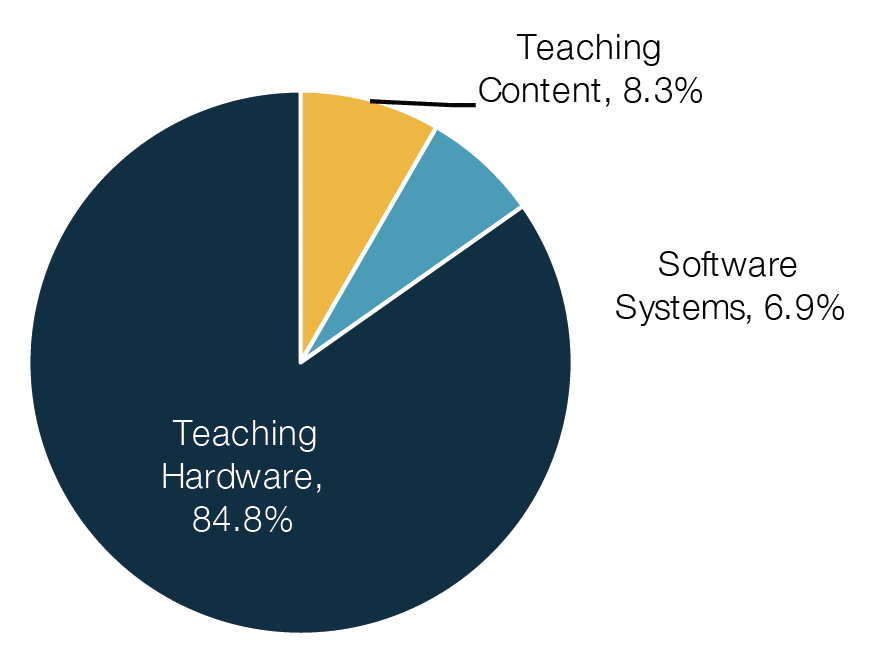

Teaching Hardware

Pandemic leads Abnormal Results

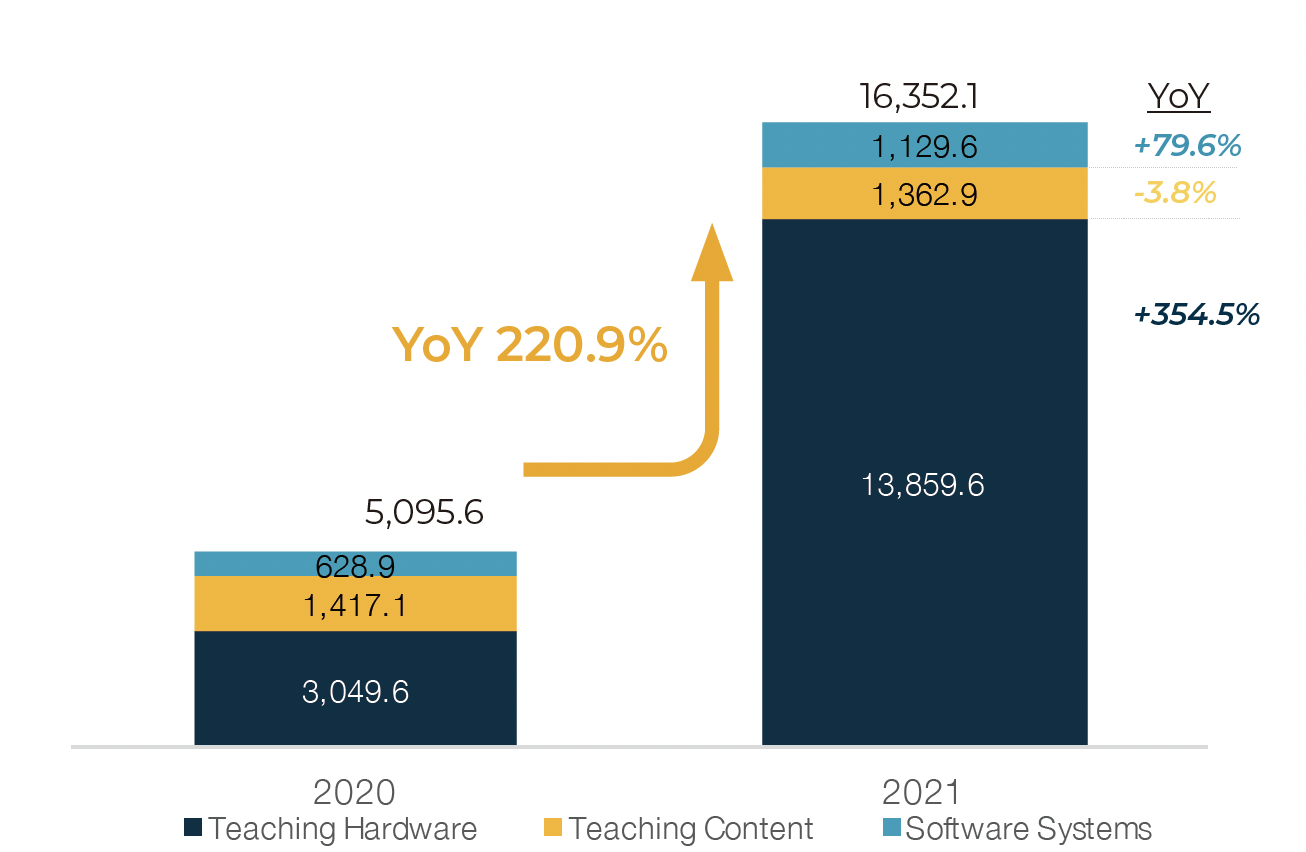

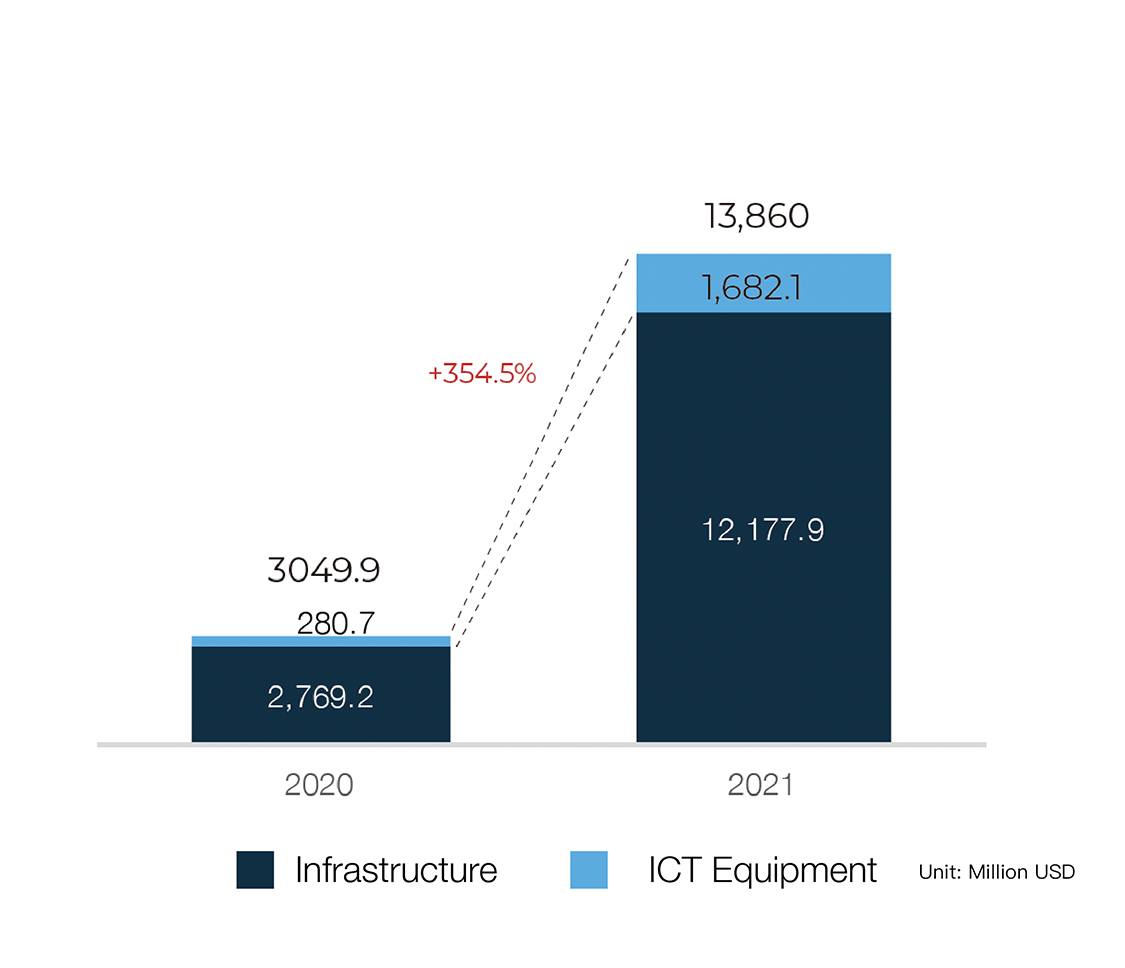

The market value of teaching hardware is US$13,860 million, which increased by 354.5% compared to the 2020 survey results. The market value of the “Information Equipment” sub-industry is US$12,177.9 million, which accounted for 87.9% of teaching hardware. The market value of the “Infrastructure” sub-industry was US$1,682.1 million, which accounted for 12.1% of teaching hardware.

The EdTech market value survey results in the past years indicated that teaching hardware has always maintained the highest ratio of the 3 categories. But the COVID-19 crisis in 2020 has shifted personal, industrial, and social operation patterns. The demands for personal teaching, learning resources, communication products, and network-related facilities have intensified this situation. This resulted in a rapid increase in the market value of teaching hardware, and the overall market value has shown “abnormal” results.